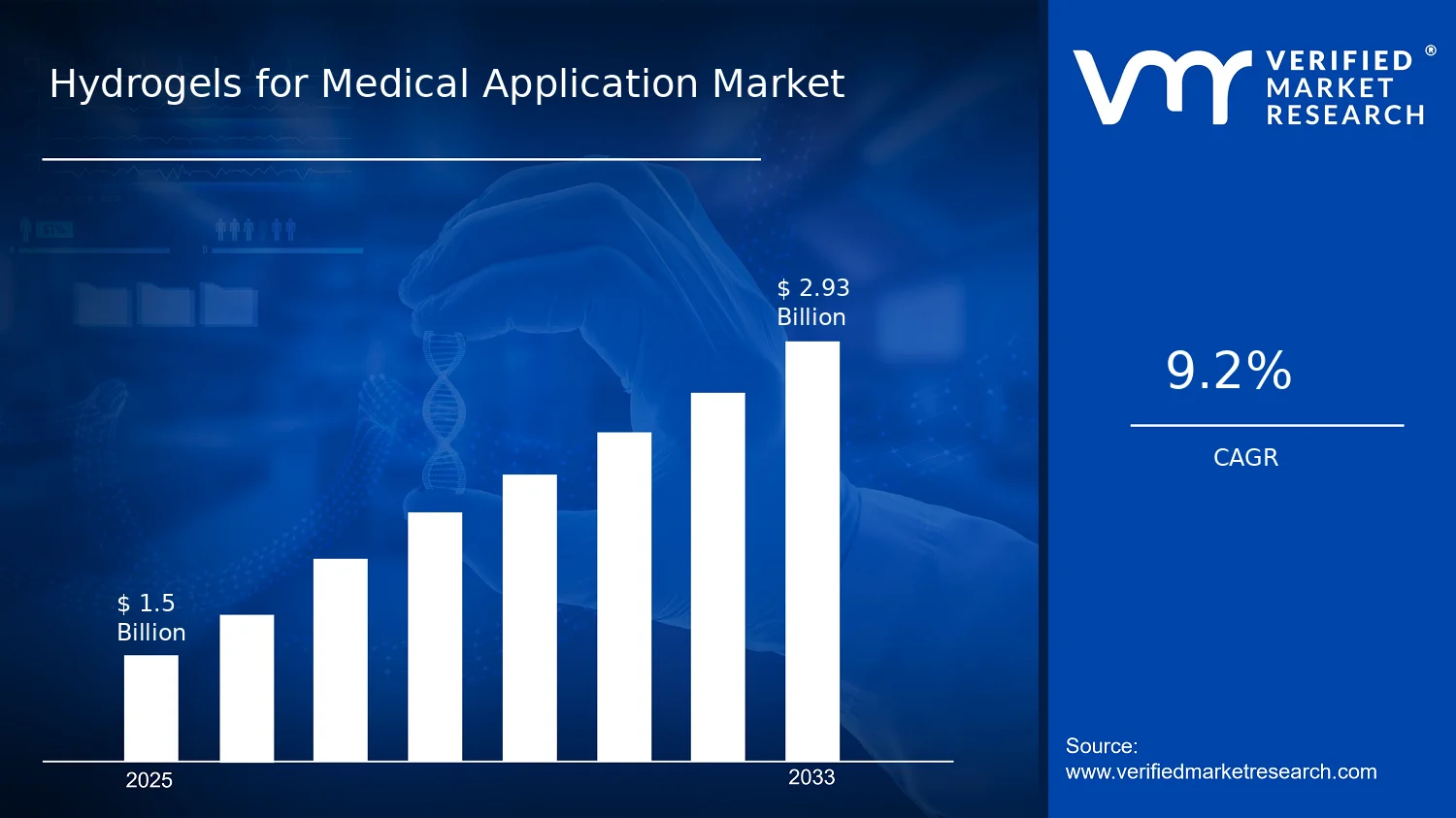

Lewes, Delaware, June 16, 2026 (GLOBE NEWSWIRE) -- Verified Market Research® has released its latest intelligence report on the Hydrogels for Medical Application Market, confirming that this dynamic sector was valued at USD 1.50 billion in 2025 and is projected to reach USD 2.93 billion by 2033, reflecting a compound annual growth rate (CAGR) of 9.2% across the forecast period. The report identifies a market advancing well beyond early adoption, transitioning into a sustained scaling phase as clinical workflows progressively integrate hydrogel-based platforms for wound care, controlled drug delivery, and tissue engineering. The expansion is grounded in structural demand dynamics from the global burden of chronic wounds to the pharmaceutical industry's intensifying emphasis on localized, efficacious therapies and is further accelerated by regulatory pathway maturation, growing biomaterials manufacturing infrastructure, and a robust pipeline of translational research.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Hydrogels for Medical Application Market Sample Report

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Hydrogels for Medical Application Market Sample Report

Market Overview: Defining the Hydrogels for Medical Application Industry

The Hydrogels for Medical Application Market encompasses the global market for hydrogel-based materials and engineered hydrogel systems that deliver clinically relevant functions in healthcare settings. Market participation is defined by offerings in which water-swollen polymer networks are intentionally designed to perform a medical role including products sold as implantable, injectable, topical, or wound contact applications along with the associated medical-grade development and system integration required to translate hydrogel chemistry into reliable clinical performance.

At the heart of the Hydrogels for Medical Application Industry lies a core requirement: hydrogels must be formulated for controlled hydration, biocompatibility, and function under physiological conditions to support medical endpoints, rather than general-purpose industrial or cosmetic uses. The market covers the material platform across natural, synthetic, and hybrid hydrogel compositions and their integration into usable formats such as pre-formed dressings, drug-loaded matrices, tissue scaffolds, and hydrogel systems engineered to support therapeutic behavior at the target site.

Importantly, the Hydrogels for Medical Application Market excludes several adjacent sectors to maintain definitional precision. Dermatological and consumer cosmetic hydrogel products where the primary objective is superficial moisturization rather than clinically targeted function fall outside scope, as do industrial hydrogel applications in agriculture, oilfield services, or non-medical absorbents. Broader pharmaceutical or biologics markets where hydrogels are not the core enabling platform are similarly excluded. These boundaries ensure that the hydrogel material and its medical functionality remain the central value driver and organizing basis for segmentation.

The global Hydrogels for Medical Application Market is organized through three primary segmentation dimensions: by type (Natural Hydrogels, Synthetic Hydrogels, and Hybrid Hydrogels), by application (Wound Care, Drug Delivery, and Tissue Engineering), and by end-user (Hospitals, Clinics, and Research Institutions). Geographic analysis spans North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Hydrogels for Medical Application Market Sample Report

Key Growth Drivers Powering the Hydrogels for Medical Application Market

Material Customization Enabling Targeted Performance

One of the most consequential drivers of Hydrogels for Medical Application Market growth is the capacity to engineer hydrogel materials for precisely targeted clinical performance. Because hydrogels can be formulated to deliver specific water retention characteristics, gel strength, permeability, and bioactivity profiles, product developers can align the material's physical behavior directly with the requirements of a given clinical need whether that is moisture management in wound dressings, controlled diffusion in drug delivery matrices, or structural integrity in tissue scaffolds.

This customization capability materially reduces trial-and-error during product development, shortening the path from formulation to regulated clinical use. As developers iterate more efficiently, new hydrogel variants enter development pipelines across wound care, drug delivery, and tissue engineering simultaneously, expanding the installed base of clinical use cases and accelerating repeat adoption across the Hydrogels for Medical Application Industry.

Expanding Clinical Adoption Through Compatibility with Modern Care Protocols

Hydrogels are increasingly recognized as controlled, moist interfaces that can integrate with complementary therapies used in contemporary wound management. Their ability to maintain a stable local healing environment can reduce treatment disruptions, lower infection risk, and improve the practicality of multi-step care protocols. As clinicians integrate hydrogel solutions into standardized care pathways particularly in high-volume hospital wound care programs and outpatient clinic workflows procurement volumes rise and conversion from pilot studies to routine clinical use accelerates, driving steady demand growth in the Hydrogels for Medical Application Market.

This driver is reinforced by the global burden of chronic wounds, with the World Health Organization noting that chronic diseases and long-term conditions continue to drive sustained healthcare needs, increasing the population at risk for wounds requiring advanced local therapies. This structural demographic pressure creates a recurring demand floor for hydrogel-based wound care products that underpins market stability even as application portfolios diversify.

Regulatory-Aligned Manufacturing Reducing Market Entry Friction

As quality expectations for medical materials tighten globally, hydrogel producers that have implemented robust controls for sterility, consistency, and batch-to-batch performance face fewer barriers in adoption cycles. This operational maturation also supports clinical evidence generation for intended use claims and enables smoother transitions from research prototypes to commercial procurement. Regulatory bodies including the U.S. Food and Drug Administration have continued to structure clear pathways for biologics and medical devices, encouraging manufacturers to generate the clinical and manufacturing data needed for broader adoption beyond early pilots.

Over time, lowered compliance friction improves market accessibility, enabling more suppliers to scale production and meet demand growth across all three application segments. The result is a virtuous cycle: better manufacturing standards lead to more consistent clinical performance, which in turn drives wider formulary acceptance in hospitals and clinics and feeds back into higher procurement volumes.

Ecosystem-Level Supply Chain Maturation

Growth in the Hydrogels for Medical Application Market is reinforced by ecosystem-level shifts in supply chain structure, manufacturing standardization, and distribution readiness. More predictable raw material inputs and improved process controls help suppliers deliver consistent material behavior, which strengthens procurement confidence for hospitals, clinics, and research institutions. Capacity expansion and consolidation among hydrogel manufacturers and specialty ingredient providers are simultaneously reducing lead times and improving product availability. These ecosystem changes enable core market drivers by lowering development uncertainty, increasing the likelihood of regulatory progression, and supporting broader geographic and institutional uptake.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Hydrogels for Medical Application Market Sample Report

Emerging Opportunities in the Hydrogels for Medical Application Market

Scaling Wound-Healing Hydrogel Offerings for Complex Chronic Conditions

A significant near-term opportunity within the Hydrogels for Medical Application Market lies in scaling wound-healing products for complex chronic ulcers, where formulary adoption remains inconsistent across regions. Hydrogel platforms capable of faster moisture balance and supportive extracellular matrix mimicry are well-positioned, yet market penetration is uneven due to limited protocol standardization and procurement inertia. Stakeholders that align product formats to clinical workflows and payer expectations particularly for chronic and recurrent wound profiles can convert underpenetrated case volumes into repeatable purchasing behavior through targeted evidence packages and modular product design.

Controlled Drug Delivery Systems with Patient-Specific Dosing Alignment

Drug delivery use-cases are expanding into territory where controlled release profiles materially affect therapeutic safety, patient adherence, and therapeutic window management. The current gap is that many hydrogel delivery systems do not fully map formulation performance to administration constraints such as residence time and depot consistency. Suppliers that develop controllable crosslinking strategies and provide clear translation of performance metrics into clinical dosing endpoints can capture demand from clinics and hospitals seeking predictable, reproducible outcomes rather than experimental device-centric approaches.

Commercializing Tissue Engineering Scaffolds at Research Scale

Tissue engineering growth is constrained by the time and cost required to iterate scaffold properties for different cell behaviors and target tissues. A substantial opportunity exists to build scalable customization pipelines using hybridizable design rules that support repeatable fabrication parameters while still enabling controlled mechanical and biological cues. Reducing scaffold turnaround time for research institutions and supporting faster progression from bench work to translational studies are critical unlocks. Hydrogels for Medical Application Market providers that operationalize customization can strengthen institutional account retention and accelerate project-to-product conversion cycles.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Hydrogels for Medical Application Market Sample Report

Market Challenges and Restraints

Regulatory Approval Timelines and Evidence Thresholds

Hydrogels for medical application must demonstrate consistent identity, biocompatibility, and performance under relevant use conditions before reaching the market. For wound care and drug delivery, regulatory bodies typically require robust clinical or equivalency evidence, while combination products introduce additional documentation complexity. These requirements extend review cycles and raise the cost of failed submissions, pushing manufacturers to postpone product launches and limit portfolio expansion. The practical result is slower diffusion across hospitals, clinics, and research institutions even when the underlying clinical demand is clear.

Production Cost Volatility and Manufacturing Process Variability

Manufacturing natural, synthetic, and hybrid hydrogels depends on sourcing, purification, and quality-critical parameters including polymer purity and gelation behavior. When supply or process variability occurs, batch-to-batch performance drift can force tighter release specifications and more expensive quality control testing. The result is higher procurement prices and operational unpredictability, creating budget friction for hospitals and clinics and reducing willingness to scale use beyond pilot programs even when clinical demand justifies broader adoption.

Performance Uncertainty in Complex Biological Environments

Hydrogels can behave differently across patient populations due to factors including infection load, enzymatic activity, hydration levels, and mechanical stress at the application site. This uncertainty is amplified when products are expected to provide multiple simultaneous functions such as moisture management, drug release, and structural support for tissue repair. When outcomes vary, clinicians may restrict use to specific patient subgroups, and procurement teams may avoid broader institutional rollout, constraining utilization rates and downstream revenue stability in the Hydrogels for Medical Application Market.

Technology and Innovation Trends Shaping the Hydrogels for Medical Application Industry

Technology is a primary determinant of capability, efficiency, and adoption across the Hydrogels for Medical Application Market. Material innovation and process refinement determine how consistently hydrogels form stable networks, maintain water management, and deliver therapeutic function under physiological conditions. From 2025 into 2033, technical evolution increasingly aligns with clinical constraints including handling time, patient safety requirements, and usability in hospitals and clinics while simultaneously expanding research-grade experimentation for drug delivery and tissue engineering.

Precision-Tuned Crosslinking for Controlled Swelling and Extended Functional Windows

Among the most impactful innovation areas is the development of crosslinking methods that achieve a better balance between water retention and structural stability. Excessive swelling or loss of mechanical integrity undermines consistency in wound coverage, scaffold support, and drug release behavior. More precise network control helps materials maintain performance as physiological conditions change fluctuating exudate levels in wound care, mechanical demands of tissue engineering, or diffusion requirements in drug delivery. The practical result is fewer variability issues across production lots and more reliable clinical performance in routine hospital and clinic settings.

Scalable Formulation and Manufacturing Controls to Reduce Batch Variability

A second innovation area addresses manufacturing discipline specifically the translation of laboratory-scale gelation into repeatable production processes. Small formulation shifts can alter viscosity, gel time, or final network density, which in turn affects product usability in clinics and compliance with medical quality expectations. Improved manufacturing controls enable tighter specification of critical material attributes and more stable preparation methods for complex constructs, particularly hybrid hydrogel systems. For hospitals and clinics, the benefit is predictable handling and consistent clinical outputs; for research institutions, it enables faster experimental iteration because material behavior becomes more controllable.

Bioactive and Hybrid Interfaces Integrating Therapeutic Function

Hydrogels are evolving toward interfaces that can engage biological targets while preserving the integrity of the surrounding polymer network. This addresses a key limitation of earlier-generation systems: adding biological functionality often compromised mechanical strength or altered release patterns in unpredictable ways. Hybrid approaches and surface-adjacent design strategies aim to maintain compatibility with tissue environments, supporting cell-surface interactions that improve outcomes in wound care and tissue engineering. In drug delivery, interface engineering helps manage how active pharmaceutical ingredients partition between the matrix and surrounding biological fluids, reducing the risk of burst release or premature loss of therapeutic efficacy.

Shift Toward Standardized Performance Characterization

Across the Hydrogels for Medical Application Market, a notable trend is the transition from material-type comparisons toward measurable, repeatable performance attributes that can be evaluated consistently by procurement teams and clinical stakeholders. Characterization is increasingly emphasizing stability, swelling behavior, biocompatibility consistency, and batch-to-batch reproducibility. As product selection becomes more protocol-linked, adoption concentrates on hydrogel formats supported by clearly documented test outcomes and predictable in-use handling. Vendors that package their evidence coherently for each application category are gaining faster uptake, while broad, undifferentiated catalog approaches face slower integration into routine workflows.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Hydrogels for Medical Application Market Sample Report

Industry Use Cases and End-User Segments

Hospitals: Protocol-Driven Procurement and High-Volume Clinical Adoption

Hospitals represent the largest and most structurally important end-user segment within the Hydrogels for Medical Application Market. As high-volume healthcare facilities managing complex wounds, chronic conditions, and post-surgical care pathways, hospitals create consistent demand for hydrogel-based dressings and delivery systems. Procurement in hospital settings is typically governed by multi-disciplinary clinical governance structures and formal purchasing frameworks that favor products supported by strong clinical documentation and standardized usage protocols. Once hydrogels are embedded in standardized wound care or drug delivery pathways, purchasing patterns shift toward higher repeat volumes, making hospital adoption a critical inflection point for market-wide scaling.

Clinics: Workflow-Integrated Adoption for Outpatient Care

Specialty clinics and outpatient care centers represent a distinct and growing demand segment, particularly for wound dressings and routine drug delivery applications. Clinic adoption is driven primarily by practical integration into workflow-based care delivery and treatment continuity. Clinics are more cost-sensitive than hospitals and have lower tolerance for operational complexity, making total cost of ownership and ease of handling decisive factors in procurement decisions. When hydrogel formulations reduce management complexity while supporting effective local healing or therapy delivery conditions, clinic purchasing decisions accelerate. As product labeling, usability, and supply reliability improve, clinic-level utilization expands faster than in settings where evidence requirements or procurement cycles are longer.

Research Institutions: Innovation Catalysts and Pipeline Development

Research institutions play a structurally different but equally critical role in the Hydrogels for Medical Application Market not as high-volume repeat buyers, but as innovation catalysts that determine the technology pipeline. These institutions adopt early-stage hydrogel systems when tuning options support experimental objectives across wound models, controlled release kinetics, and scaffold behavior. Because research adoption translates into stronger downstream demand by informing translational partners and accelerating evidence generation toward clinical procurement, it is a leading indicator of future market growth. Suppliers that provide robust documentation and configurable formulations for research environments capture institutional relationships that often become the foundation for broader clinical partnerships.

Wound Care Applications: Recurring Demand from Chronic Conditions

Wound care remains the most established application segment within the Hydrogels for Medical Application Market and provides dependable baseline demand driven by high clinical need and repeat treatment cycles. Hydrogel dressings are applied directly to wound surfaces during scheduled dressing changes, where their functional role is to regulate moisture, protect the wound surface, and interact with the healing process in a controlled manner. The operational requirements extend beyond basic biocompatibility to include stability under exudate conditions and the ability to remain effective without complicating clinical handling. As health systems seek consistent performance across varying wound types and patient profiles, procurement emphasis is shifting toward products that reduce outcome variability during routine application.

Drug Delivery Applications: Controlled Release Enabling Precision Therapy

Drug delivery represents a rapidly evolving application segment where the hydrogel's role is not immediate handling but predictable therapeutic function over time. Injectable or conformable hydrogel formats are positioned so that active pharmaceutical ingredients remain at or near the target site long enough to support a defined dosing regimen. Key evaluation criteria include predictable diffusion through the gel network, compatibility with specific therapeutics, and robustness during administration. As clinicians and developers increasingly seek reduced dosing frequency and improved local bioavailability, the Hydrogels for Medical Application Industry is responding with synthetic and hybrid systems that offer engineered transport and release profiles, tighter formulation-to-function documentation, and clearer clinical endpoint mapping.

Tissue Engineering Applications: Scaffold Performance for Regenerative Medicine

Tissue engineering represents the highest-complexity and highest-growth-potential application within the Hydrogels for Medical Application Market. Hydrogel systems are deployed as structural and bioactive materials that support cell growth, tissue formation, or regenerative pathways, functioning as three-dimensional scaffolds within which cells can attach, proliferate, and organize. The operational constraints are distinct from wound or delivery scenarios: constructs must tolerate sterilization, maintain structural integrity during handling, and provide surface and mechanical cues that support cell maturation over the course of culture or implantation. Research institutions are the primary early adopters in this segment, with clinical translation progressing as scaffold performance is validated under increasingly realistic biological conditions.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Hydrogels for Medical Application Market Sample Report

Regional Outlook: Hydrogels for Medical Application Market by Geography

North America: Innovation-Led Demand and Rapid Clinical Integration

North America holds a leading position in the global Hydrogels for Medical Application Market, characterized by innovation-led demand and a high concentration of end-users that actively test and implement new hydrogel modalities. The region's hospital procurement structures and advanced care infrastructure create a faster feedback loop between clinical outcomes and product iterations. Regulatory compliance functions as a practical driver, as manufacturers align material characterization, biocompatibility testing, and quality systems to meet U.S. requirements, reducing procurement uncertainty for enterprise buyers.

Key factors shaping North America's market position include dense biomaterials innovation ecosystems encompassing universities, translational research groups, and specialized suppliers working on crosslinking strategies and drug-loading techniques; robust venture funding that enables frequent product development milestones including clinical readiness work and manufacturing capability upgrades; outcome-based procurement evaluation that incentivizes manufacturers to target specific, measurable performance claims; and mature medical-grade supply chains that reduce restocking delays for wound care protocols and research workflows.

Europe: Regulation-Led Adoption and Quality-Driven Market Structure

Europe's position in the Hydrogels for Medical Application Market is shaped by regulation-led adoption, where product development, manufacturing controls, and clinical use are governed by EU-wide expectations for safety, traceability, and quality management. This discipline affects every segment from natural hydrogels to hybrid systems because harmonized technical requirements raise the cost of non-compliance and compress acceptable development paths for riskier formulations. The region's industrial base is tightly integrated across borders through shared supply chains and certified logistics, supporting consistent access to raw materials and finished medical products.

Sustainability and environmental constraints increasingly reshape European supply chains, particularly where natural and hybrid hydrogels depend on bio-derived inputs or specific processing solvents. Cross-border market integration allows suppliers to scale distribution faster when regulatory and documentation frameworks are consistently met, but it simultaneously raises the baseline for technical documentation including performance evidence, risk management outputs, and labeling alignment across jurisdictions. The practical effect is a market that favors incremental but credible innovation over high-uncertainty material claims.

Asia Pacific: High-Growth Expansion Driven by Population Scale and Manufacturing Build-Out

Asia Pacific is positioned as a high-growth, expansion-driven region within the Hydrogels for Medical Application Market, shaped by the contrast between highly mature healthcare and manufacturing ecosystems in Japan, Australia, South Korea, and Singapore, and faster infrastructure-led scaling in India and Southeast Asian economies. The region's population scale amplifies baseline demand for wound care and drug delivery, while rapid urbanization supports higher patient throughput in hospitals and expanding clinic networks.

Cost-competitive production and localizing supply chains reduce barriers to adoption for synthetic and hybrid hydrogel formulations. However, the market remains structurally fragmented, with differences in reimbursement structures, procurement pathways, and industrial capacity influencing demand momentum across countries. Regulatory variability across jurisdictions shapes how quickly hydrogel technologies move from clinical trials to routine use, while government-backed healthcare and manufacturing initiatives can accelerate ecosystem development, with research institutions often forming the initial commercialization bridge.

Latin America: Emerging Growth Concentrated in Major Economies

Latin America represents an emerging but gradually expanding segment within the Hydrogels for Medical Application Market, with demand concentrated in Brazil, Mexico, and Argentina. Adoption is shaped by economic cycles that affect purchasing power and procurement timing, while currency volatility can alter landed costs for hydrogel inputs and consumables. The region's developing industrial base and uneven healthcare infrastructure influence how quickly wound care solutions, drug delivery platforms, and tissue engineering materials progress from pilot programs to routine clinical use.

Key constraints include currency-driven demand fluctuations that create stop-and-go procurement patterns, import and supply-chain dependency that raises vulnerability to logistical disruptions, and regulatory and policy inconsistency across countries that extends time-to-market for new formulations. Selective increases in foreign investment and vendor partnerships are supporting pilot-to-commercial transitions in larger urban centers and higher-acuity hospital networks, with wound care applications typically reaching wider adoption before advanced tissue engineering systems.

Middle East & Africa: Selectively Developing Demand Anchored in Gulf Economies

The Hydrogels for Medical Application Market in the Middle East and Africa is evolving as a selectively developing region rather than a uniformly expanding one. Gulf economies including the UAE, Saudi Arabia, and Qatar shape demand through healthcare modernization initiatives and hospital-led procurement cycles, while South Africa acts as a more established anchor for clinical adoption and local research activity. Policy-led industrial and healthcare diversification in select countries supports earlier adoption of advanced biomaterials, but the broader region faces structural limitations including healthcare infrastructure gaps, import dependence, and cross-border regulatory inconsistency that slow diffusion beyond major urban and academic hubs.

Healthcare infrastructure gaps across African markets influence how quickly hydrogel-based solutions move from research and trial use to repeat purchasing. While urban hospitals and select clinics can support standardized wound management and post-surgical protocols, peripheral regions face constraints in supplies, trained staff, and device compatibility. Demand formation is therefore strongest in major metropolitan areas, with drug delivery adoption tending to cluster around institutions with stronger procurement governance. Wound care applications typically achieve commercial stability first, with advanced regenerative use cases maturing later across the forecast horizon.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Hydrogels for Medical Application Market Sample Report

Competitive Landscape: Key Players in the Hydrogels for Medical Application Market

The Hydrogels for Medical Application Market competitive structure is best characterized as moderately fragmented, with competition split between large medical device groups and specialized wound and regenerative therapy specialists. The intensity of rivalry is driven less by headline pricing and more by performance evidence, regulatory compliance, biocompatibility validation, and the ability to scale manufacturing without introducing variability in critical hydrogel attributes such as gel strength, diffusion behavior, and degradation profiles.

- Johnson & Johnson - Operates as an integrator with strength in clinical pathway adoption and broad access to healthcare settings. Its competitive influence on the Hydrogels for Medical Application Market comes from integrating hydrogel-based solutions into larger therapeutic and procedural frameworks, where compliance, consistent product performance, and clinician familiarity determine switching decisions. Large-scale manufacturing and procurement discipline set practical benchmarks for supply continuity and documentation readiness.

- 3M Company - Competes by leveraging manufacturing process discipline and strong capabilities in medical materials where product performance and handling characteristics are decisive. In wound care delivery, 3M differentiates through materials science execution and formulation control, enabling hydrogels to be engineered for stable performance under real-world conditions. Its scale influence is most visible in supply robustness and consistent quality, which reduces operational risk for hospitals and procurement teams.

- Smith & Nephew PLC - Positions as an applications-focused medical technology company, shaping competition through integrated wound-care offerings and workflow-aligned technologies. Differentiation is driven by portfolio orchestration, where hydrogel solutions are positioned as more valuable when paired with complementary products and clinical usage protocols. The company's emphasis on evidence generation and clinician education affects formulary decisions and standard of care adoption.

- Integra LifeSciences Corporation - Functions primarily as a specialist integrator in surgical and tissue-focused solutions, with competitive impact driven by how hydrogel-enabled technologies can support advanced healing and procedural compatibility. Its positioning aligns with tissue engineering-adjacent needs where hydrogel performance depends on biological compatibility, predictable degradation, and fit within operative workflows.

- Medtronic PLC - Competes through systems engineering and translational capabilities that connect hydrogels to medical device contexts, including pathways relevant to drug delivery and longer-term therapeutic interfaces. Its role reflects converting hydrogel characteristics into device-compatible performance criteria such as controlled release behavior, stability, and integration with delivery or monitoring technologies.

- Additional participants including Coloplast A/S, ConvaTec Group PLC, Organogenesis Inc., MiMedx Group Inc., and Acelity L.P. Inc. collectively shape competition through specialization in wound-care routes, regional reach in care settings, and application-specific portfolios.

Looking ahead to 2033, the Hydrogels for Medical Application Market is expected to evolve toward greater differentiation by system-level performance, with moderate consolidation risk concentrated in manufacturing scale and evidence capabilities. Specialization in hydrogel formulations and application fit is expected to remain a durable competitive strategy, particularly in drug delivery and tissue engineering where performance requirements are most stringent.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Hydrogels for Medical Application Market Sample Report

Market Segmentation Overview

By Type

- Natural Hydrogels -Align with biocompatibility and cell-interactive performance needs, with adoption frequently concentrated in wound care environments and tissue-facing scaffolds in tissue engineering. Manufacturing requires tight process controls to manage lot-to-lot consistency.

- Synthetic Hydrogels -Positioned around engineered reliability and tunable properties, including controlled gelation, permeability, and degradation profiles. Particularly relevant for controlled drug delivery constructs and standardized tissue engineering scaffolds where reproducibility is a primary requirement.

- Hybrid Hydrogels -Capture value where performance needs combine biological affinity with engineered structural control. Positioned to serve use cases that require both biofunctionality and mechanical reliability, supporting distributed adoption across multiple applications.

By Application

- Wound Care -Provides dependable baseline demand driven by high clinical need and repeat treatment cycles. Hydrogels are assessed primarily for how they manage moisture, protect wound surfaces, and interact with healing processes. Adoption is embedded in recurring clinical care schedules.

- Drug Delivery -A rapidly evolving segment where hydrogels function as delivery platforms governing loading, retention, and release of therapeutics to defined target environments. Growth is driven by demand for controlled release profiles that align with clinical dosing strategies and reduce systemic exposure.

- Tissue Engineering -Positions hydrogels as structural and bioactive materials supporting cell growth, tissue formation, or regenerative pathways. This segment shows the fastest evolution in product complexity, creating pockets of concentrated growth as technical performance improves and clinical evidence accumulates.

By End-User

- Hospitals -Anchor a larger share of the market through repeat usage in clinical care pathways and protocol-based procurement. Purchasing emphasizes risk management, supply reliability, and documentation depth.

- Clinics -Shape demand through practical outpatient application needs. Adoption is governed by workflow fit, ease of use, and total cost of ownership, with steady expansion potential where product formats are standardized.

- Research Institutions -Influence upstream material innovation and the technology pipeline that later moves into clinical environments. Early adopters of novel hydrogel architectures that subsequently translate into commercial procurement.

By Geography

- North America -Innovation-led demand, regulatory compliance maturity, and high end-user concentration drive the fastest adoption cycles.

- Europe -Regulation-led adoption with standardized evaluation pathways; quality and sustainability constraints shape product development priorities.

- Asia Pacific -High-growth expansion driven by population scale, manufacturing build-out, and infrastructure investment; structurally fragmented by country-level differences.

- Latin America -Emerging, gradually expanding demand concentrated in Brazil, Mexico, and Argentina; constrained by economic cycles and import dependency.

- Middle East & Africa -Selectively developing, anchored in Gulf healthcare modernization programs and South African research capacity.

Download a free sample to access exclusive Insights, Data Charts, And Forecasts From Hydrogels for Medical Application Market Sample Report

Investment and Funding Activity in the Hydrogels for Medical Application Market

The investment landscape in the Hydrogels for Medical Application Market shows capital concentrated on translational and commercialization pathways rather than early-stage platform exploration alone. Recent activity reveals investor confidence that hydrogel modalities can clear clinical and regulatory hurdles, with funding allocated across wound repair, injectable regenerative scaffolds, and cartilage and tissue repair programs.

Notable examples include a USD 20 million oversubscribed Series A supporting commercialization of an FDA-cleared dermal regeneration hydrogel backed by both strategic and clinical stakeholders; a USD 12 million Series A advancing a synthetic tissue scaffold technology platform for complex surgical site reinforcement; and a USD 13 million seed financing for an injectable hydrogel scaffold approach tied to a retinal pigment epithelial cell therapy program that also included a strategic collaboration with a pharmaceutical organization for stem-cell derived therapies.

Funding rounds across the Hydrogels for Medical Application Industry show consistent participation by entities with clinical, manufacturing, and development capabilities beyond purely financial sponsors. This syndication behavior signals a market preference for projects capable of moving efficiently from prototype to clinical protocol, then into commercial adoption through trial design support and regulatory readiness. Capital allocation patterns indicate that regulatory progress, clinical trial readiness, and partner-enabled commercialization are the primary gating factors for follow-on investment.

Strategic Outlook: Hydrogels for Medical Application Market Through 2033

The Hydrogels for Medical Application Market is entering one of its most consequential growth phases, with the trajectory from USD 1.50 billion in 2025 to USD 2.93 billion by 2033 representing not merely incremental unit sales but a fundamental shift in how hydrogel-based platforms are integrated into clinical infrastructure globally. The market's 9.2% CAGR reflects a blend of adoption of established wound care categories and the gradual scaling of newer drug delivery and tissue engineering modalities as they move from research protocols toward routine clinical use.

From a maturity perspective, the market is best characterized as in an expansion-to-scaling transition. Demand is broadening across end-user settings from hospital formularies to outpatient clinics and academic research centers -while the application mix is widening from primarily wound-oriented use cases toward multi-therapy platforms. This pattern is consistent with an industry that is simultaneously increasing penetration in established categories and diversifying into higher-complexity performance requirements.

The most robust competitive positions through 2033 are expected to accrue to suppliers capable of spanning multiple hydrogel chemistries and tailoring formulations to application-specific requirements -particularly for drug delivery and tissue engineering where system performance requirements are most stringent. Meanwhile, clinical demand in wound care continues to support volume stability, enabling material and manufacturing investments that can extend into higher-value modalities over time.

Technology evolution over the forecast period will increasingly align with the dual imperatives of clinical practicality and research-grade performance: precision crosslinking for more dependable functional windows, scalable manufacturing controls for consistent lot quality, and bioactive interface engineering for broader application scope. Together, these capabilities will determine which platforms achieve the fastest path from development to regulated clinical adoption and, ultimately, which organizations capture the growing value available in the global Hydrogels for Medical Application Market.

Related Reports

Global Hydrogels for Tissue Engineering Market Size By Product Type (Natural Hydrogels, Synthetic Hydrogels), By Material Type (Collagen-based Hydrogels, Hyaluronic Acid-based Hydrogels), By Application (Regenerative Medicine, Wound Healing), By Geographic Scope And Forecast

Global 3D Bioprinting and Bioink Market Size By Material (Hydrogels, Living Cells, Extracellular Matrices), By Application (Tissue Engineering, Drug Testing and Development, Regenerative Medicine), By End-User (Research Organizations, Biopharmaceutical Companies, Hospitals), By Geographic Scope And Forecast

Global Bioactive Dressings Market Size By Product Type (Skin Substitute, Hydrogels), By Property Type (Non-Antimicrobial Dressings, Antimicrobial Dressings), By Application (Chronic Wounds, Acute Wounds), By End-User (Hospitals And Clinics, Ambulatory Surgical Centers), By Geographic Scope And Forecast

Global Hydrogel Market Size By Raw Material Type (Synthetic Hydrogels, Natural Hydrogels, Hybrid Hydrogels), By Composition (Polyacrylate, Polyacrylamide, Silicone-modified Hydrogels, Agar-based), By Application (Agriculture, Health Care and Hygiene, Contact Lenses), & By Geographic Scope And Forecast

How CRISPR Screen Technology Is Transforming Drug Target Discovery in 2026

Visualize Hydrogels for Medical Application Market using Verified Market Intelligence -:

Verified Market Intelligence is our BI Enabled Platform for narrative storytelling in this market. VMI offers in-depth forecasted trends and accurate Insights on over 20,000+ emerging & niche markets, helping you make critical revenue-impacting decisions for a brilliant future.

VMI provides a holistic overview and global competitive landscape with respect to Region, Country, Segment, and Key players of your market. Present your Market Report & findings with an inbuilt presentation feature saving over 70% of your time and resources for Investor, Sales & Marketing, R&D, and Product Development pitches. VMI enables data delivery In Excel and Interactive PDF formats with over 15+ Key Market Indicators for your market.

About Us

Verified Market Research® stands at the forefront as a global leader in Research and Consulting, offering unparalleled analytical research solutions that empower organizations with the insights needed for critical business decisions. Celebrating 10+ years of service, VMR has been instrumental in providing founders and companies with precise, up-to-date research data.

With a team of 500+ Analysts and subject matter experts, VMR leverages internationally recognized research methodologies for data collection and analyses, covering over 15,000 high impact and niche markets. This robust team ensures data integrity and offers insights that are both informative and actionable, tailored to the strategic needs of businesses across various industries.

VMR's domain expertise is recognized across 14 key industries, including Semiconductor & Electronics, Healthcare & Pharmaceuticals, Energy, Technology, Automobiles, Defense, Mining, Manufacturing, Retail, and Agriculture & Food. In-depth market analysis cover over 52 countries, with advanced data collection methods and sophisticated research techniques being utilized. This approach allows for actionable insights to be furnished by seasoned analysts, equipping clients with the essential knowledge necessary for critical revenue decisions across these varied and vital industries.

Verified Market Research® is also a member of ESOMAR, an organization renowned for setting the benchmark in ethical and professional standards in market research. This affiliation highlights VMR's dedication to conducting research with integrity and reliability, ensuring that the insights offered are not only valuable but also ethically sourced and respected worldwide.

Follow Us On: LinkedIn | Twitter | Threads | Instagram | Facebook

Mr. Edwyne Fernandes Verified Market Research® US: +1 (650)-781-4080 US Toll Free: +1 (800)-782-1768 Email: sales@verifiedmarketresearch.com Web: https://www.verifiedmarketresearch.com/ SOURCE – Verified Market Research®

![]()